Most people who dream of buying a house usually will begin by scouring sites like Zillow for their dream home. If one comes up that they are interested in enough, people often call the listing agent, or another agent they know, to go see the house. Is this the best way to begin the home buying process?

This is certainly not a bad way to start the process. However, if you find your dream home on the internet and then fall in love with it in person, it can be somewhat devastating to learn that you may not be comfortable with or able to make the monthly payment. With this in mind, I would urge everyone to speak with a bank before getting too invested in the search process. Furthermore, you will need to have a pre-approval letter from a bank to make an offer on a property. In Harrisonburg/Rockingham's current market, desirable houses that are priced well do not last long. Should your perfect house come on the market, you will want to have the ability move quickly. For perspective, I have recently sold two houses before they hit the market. So, having your pre-approval letter ready to go is vital. If you or someone you know is looking to star the home buying process, contact me for recommendations on lenders and next steps: Phone or email.

0 Comments

Many investors will argue different sides on this topic. Some investors will say that more cash flow with a 30 year mortgage is more advantageous because it frees up your money to do what you please, including reinvest. While other investors will argue that you pay less interest with a 15 year mortgage. Also, you pay the loan off more quickly and at that point get more cash flow. So is there a clear answer? I have my opinions but I think that looking at the numbers will be more helpful. To help see the numbers, lets create a hypothetical rental that you are purchasing and how the numbers play out on a 15 year note and a 30 year note. Purchase Price: $144,000 Down Payment: $28,800 Loan Amount: $115,200

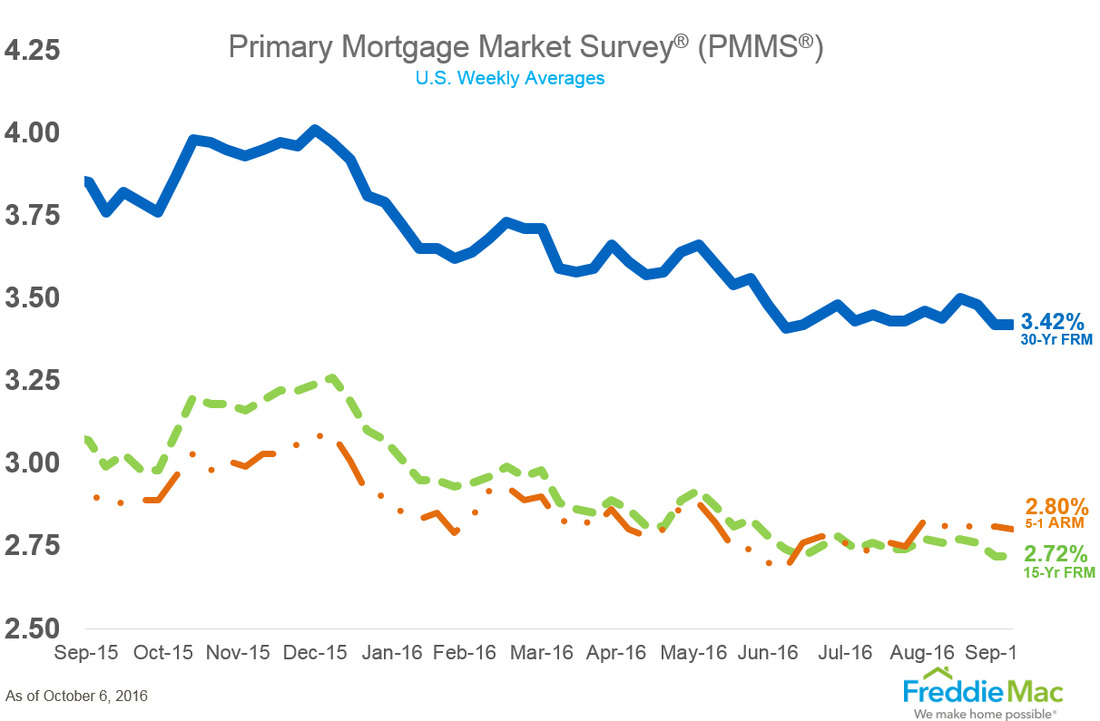

I think a hybrid approach can also be a good approach if you have the discipline. That is, put the loan on a 30 year note but pay it down on a 15 year schedule. This way, should you need more flexibility one month, you are able access more of the cash flow. So what are your thoughts? Comment below as to what you think is the best route to take. If you are looking to buy a house you will most likely need to apply for a mortgage. To do so, you will need to go through the application process. This article will help you understand what you will need. Paycheck Stubs A Mortgage adviser will ask you to prove your last month of pay by providing two pay stubs. W-2s You will also need to provide your 2 most recent W-2 forms. Bank and Investment Documentation Your mortgage adviser will ask you to provide bank and investment statements for the past 30-90 days. Depending on your situation, you may be asked provide a few additional documents. Contact me if you would like local suggestions.   As you can see, rates have been hovering for the past few months. One of the clear advantages of today's market is being able to borrow at rates this low. This will save you a lot of money whether you are looking ot buy your primary residency or an investment.

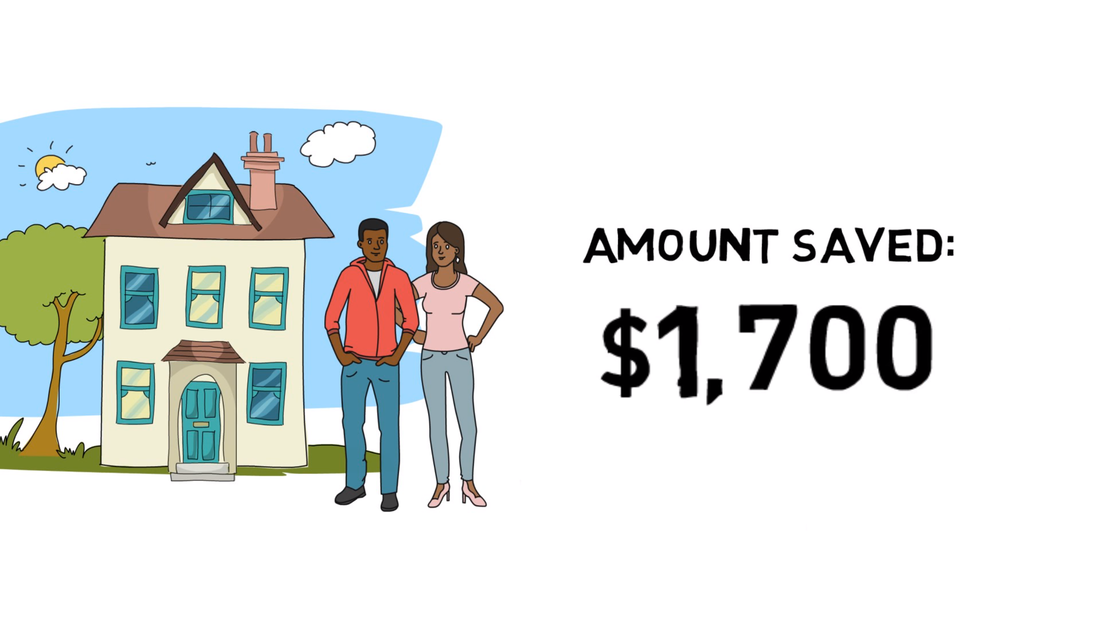

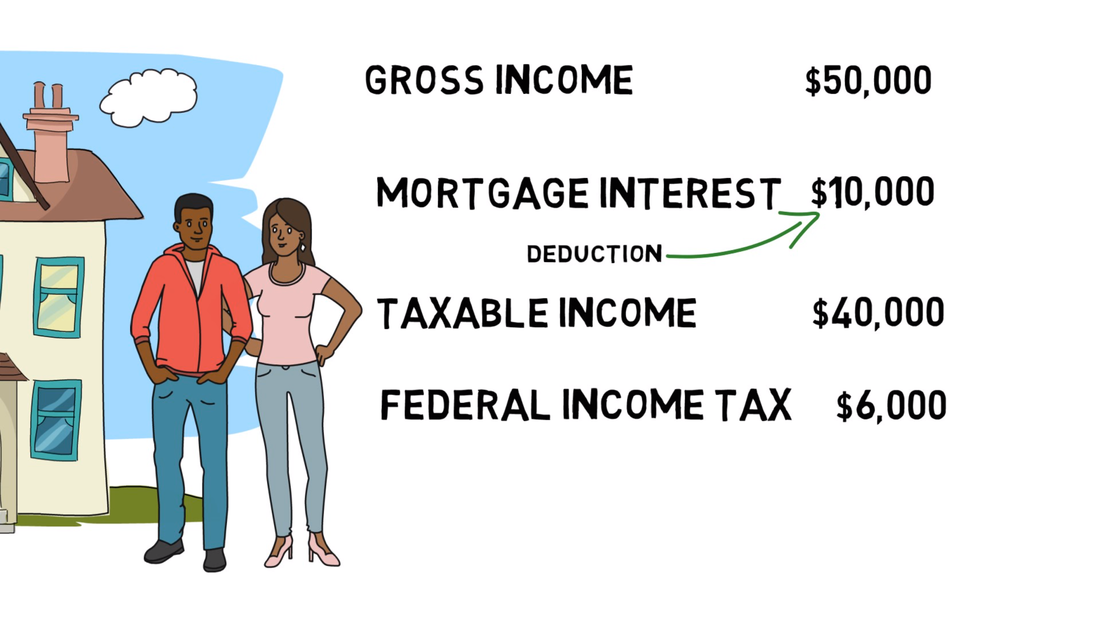

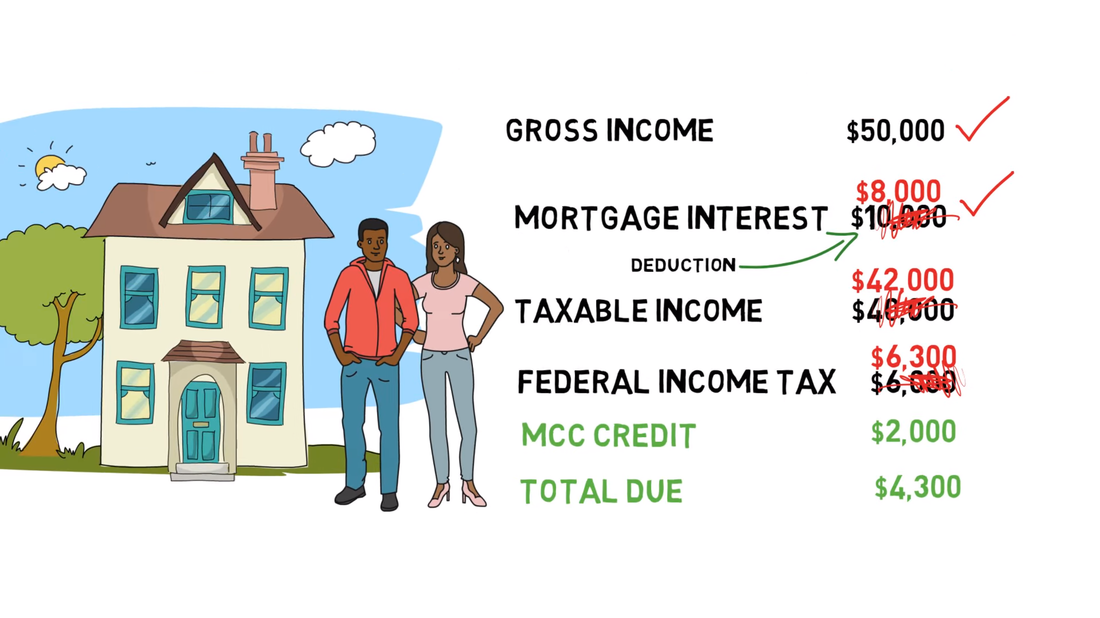

If you want recommendations on excellent local mortgage advisers, call me at 540-246-9067.  If you are a first time homeowner, or not owned a home as your primary residence for the past 3 years, you could be able to benefit significantly from a VHDA Mortgage Credit Certificate (MCC). How much? It's actually significant. Most people will take the interest they pay on their mortgage and deduct that from their taxable income. So, they wont pay taxes on the money earned that went to the mortgage interest. These savings depend on the tax bracket you are in. The MCC credit will let you take 20% of the interest you pay off of your total tax bill. You are then able to deduct the rest of the interest in the normal way. The video below spells out the savings pretty well. If you don't want to watch it, here are some screen shots that will explain the savings.  This is what the normal deduction would look like. They are simply reducing their gross income by the interest they paid on their mortgage. This leaves them owing $6,000 in tax. Now lets look at how their taxes would look like with an MCC credit.  Here we can see that their income and mortgage interest are still the same. However, they are only able to reduce their taxable income by 80% of the mortgage interest they paid because the other 20% is being applied through the MCC credit. As you can see, the total taxes they owe are $1,700 less with the MCC. If you are interested, be sure to watch the video below. Also check out VHDA's website for more information:  There has been a lot of hype surrounding the change of the settlement documents. As you can read in my previous blog, a lot of people were predicting worst case scenarios. Now that the change is here, what has actually happened? What as a consumer do we actually need to know?

There can be a lot of factors that go into play when selecting a mortgage adviser. You ultimately want an adviser who will find you the lowest and most reliable rate. It may help you to ask your friends and family as to who they recommend. In addition, asking other real estate professionals, such as myself, can be helpful when selecting a mortgage adviser.

Be sure your mortgage adviser knows and understands the property or area in which you intend on purchasing. This can be very important in order to ensure there are no surprises before closing. Here are two of my recommendations: Chris Carson Integrity Home Mortgage Corp (540) 333-2095 [email protected] Joe Slagell Park View Federal Credit Union (540) 437-7408 [email protected]  If you are not familiar with the new closing documents, named TILA RESPA Integrated Documentation (TRID), that were supposed to come on August 1st, check out my blog that describes them and the delays that were expected.

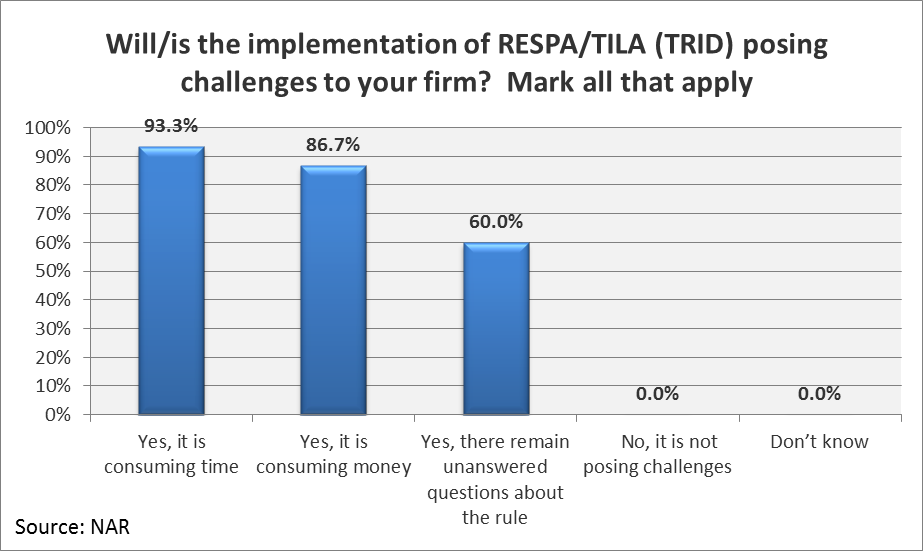

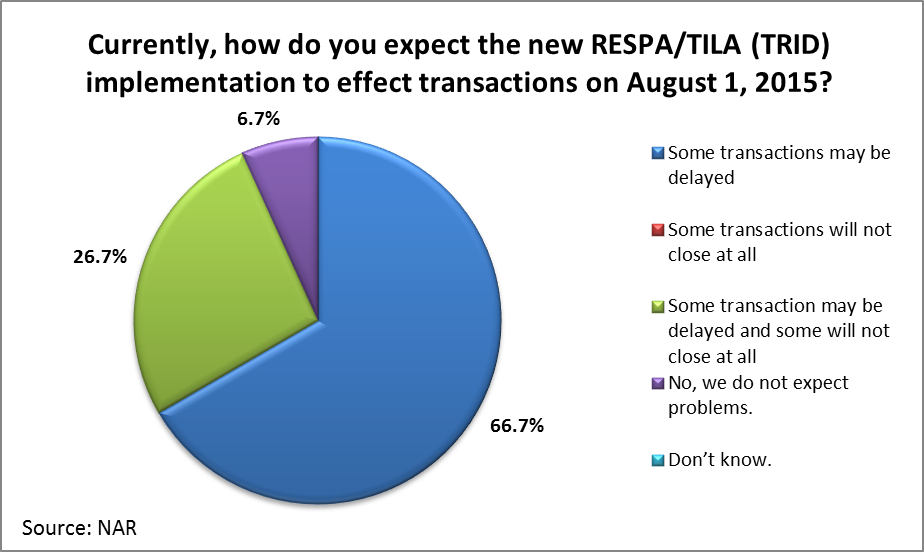

Just as in Mathematics, do two negatives (delays) make a positive? That is just what the Consumer Financial Protection Bureau is hoping by delaying TRID to October 1st. As you can see in my previous blog entry listed above, a lot of mortgage institutions were expecting delays in closings and were even apprehensive that some transactions would not close at all. As the deadline approached, the National Association of Realtors and the lending institutions grew increasingly concerned as their software was not on track for a timely integration in preparation for the change. So, if you were planning to close in August, you can be assured that your closing will not be affected by the new closing forms. The question stands: Will there be enough time to make a smooth transition in October? Will there still be delays in closings? The Consumer Financial Protection Bureau is requiring all lenders to begin using new closing documents on August 1st. The new documents are an attempt to make the process smoother and offers more consumer protections. The short hand for these forms are TILA RESPA Integrated Documentation. The even shorter hand is TRID. As with any change, there are people who welcome the adoption and there are people who are more hesitant to change. Regardless of personal preferences surrounding change, what are the logistics of this upcoming change? How are lenders affected by this process? And what will this mean for the consumers? The NAR asked lenders these questions in the 1st quarter Survey of Mortgage Originators. Unsurprisingly, the survey found that lenders were spending time and money to be in compliance with the change. In addition, 60% of those surveyed said that they still have unanswered questions.  The majority of of lenders state that they expect some transactions to be delayed. More shockingly, 26.7% percent of lenders surveyed think that some transactions will be delayed and some will not close at all.  It is important to keep in mind that these stats are coming from opinions of mortgage originators. As mentioned earlier, everyone has their own perspective on change which influence their perception of how this may play out. I would venture to say that while these changes may cause short term delays, they will not have significant impacts on the real estate market long term. Source: Realtor.org

Are you considering buying your first house? You are probably wondering how much money you will need to invest in your first home.

While, each mortgage program is different and the money you will need also depends on the house you buy, I can break things down for you to give you an idea. In most cases, there are three major expenses that you will need to include in your calculations: Earnest money, down payment, and closing costs. Earnest Money Earnest money is essentially a deposit upon making an offer. This deposit displays how serious you are in buying the house. This money will go towards your closing costs and/or down payment at closing. However, if you decide to walk away from the contract (in a way that is not supported in the contract) this money could be disbursed to the seller. Feel free to ask me for more information on how to protect earnest money when making an offer. How much? This varies greatly in different markets. In Rockingham county, it somewhat depends on the purchase but between $500 and $2,000 is common. One way to strengthen your offer is by offering higher amounts of earnest money. Down Payment The down payment really depends on the type of mortgage you go with. This is best explained in detail by a mortgage adviser, contact me for my recommendations. At the moment, you can get a house with as little as 3% down. If you don't put 20% down on a house, you will likely pay PMI (Private Mortgage Insurance) until you have 20% equity in the house. Closing Costs Again, closing costs can vary. In Virginia, the Realtor fees are paid by the seller. The buyer is responsible for paying the costs associated with processing the paperwork. This can be around 3-4% of the purchase price. However, talk to a mortgage adviser for a better estimate given your price range. Buyers commonly ask for sellers to cover closing costs as part of the negotiation. Keep in mind that this expense directly affects what the sellers net. |

Categories

All

|

RSS Feed

RSS Feed

|

Email - Click Here

Phone - 540-246-9067 Website - www.mattiasclymer.com Schedule a Meeting, Download Contact Card, Etc... |

Funkhouser Real Estate Group | 401 University Boulevard, Harrisonburg, VA 22801 | 540-434-2400 | ©2021 | Privacy Policy | All rights reserved.

Licensed in the Commonwealth of Virginia